Business entities with significant R&D budgets should be prepared for tax law changes effective in 2022.

Although the Tax Cuts and Jobs Act (TCJA) was signed into law in December 2017, several provisions did not take effect for several years. Among them are significant changes around the treatment of research and development (R&D) expenses. Before 2022, businesses were permitted to fully expense the costs of R&D. However, effective Jan. 1, 2022, those expenses may no longer be eligible for an immediate deduction but are to be amortized over five years (for domestic R&D) or even 15 years (for foreign R&D spend)[1].

These amortization requirements increase taxable income and thereby reduce cash flow. The cash flow impact can be significant, especially for Software as a Service (SaaS), technology, life sciences and other companies that conduct a significant amount of R&D. The tax bite will be even bigger for those business entities with significant R&D spend outside the U.S.

Want the big picture on 2025 tax changes?

President Trump’s “One Big Beautiful Bill” (OBBB) reshaped U.S. tax policy with major reforms for individuals, businesses, and international transactions. From deductions to depreciation, estate planning to opportunity zones, the OBBB impacts nearly every taxpayer. Read our full overview of the OBBB’s tax provisions.

Example

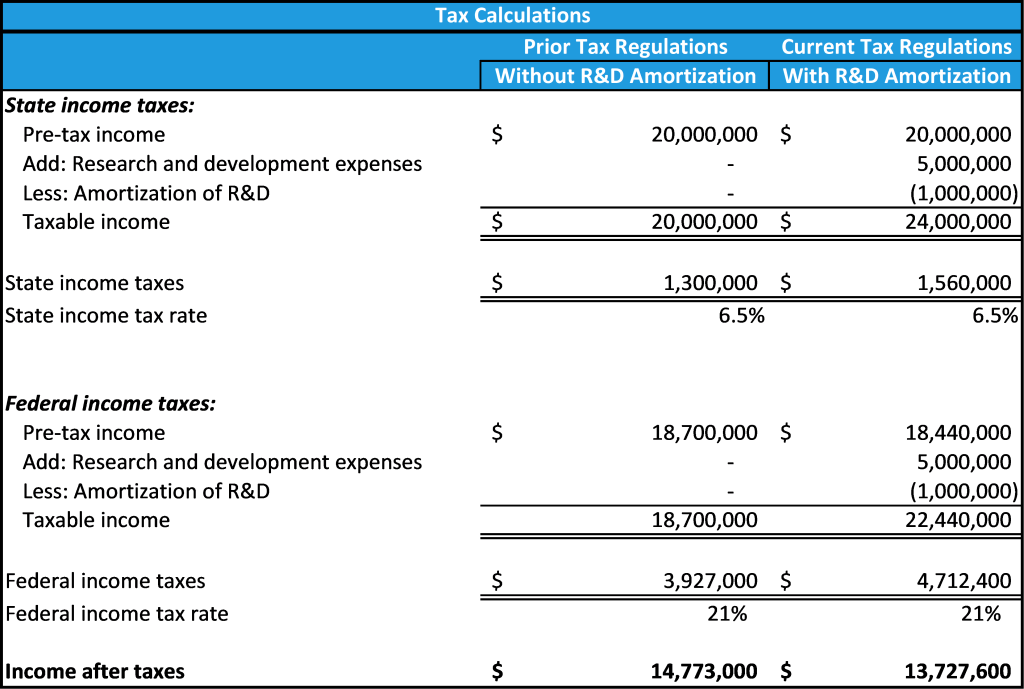

ACME Company, our hypothetical client, is a SaaS company providing the leading business enterprise solution in its industry. For simplicity purposes, let’s assume there are no working capital requirements, no equipment to be purchased or depreciated, and no intangible assets to be amortized. With revenues of $50MM, $5MM in R&D spending, and a 40% EBITDA margin, its net income (using prior tax regulations) is $14.77MM. However, once the TCJA provisions are considered, tax obligations increase and net income declines to $13.73MM, a million dollar impact (see Exhibit 1)

Exhibit 1

Impact on Value

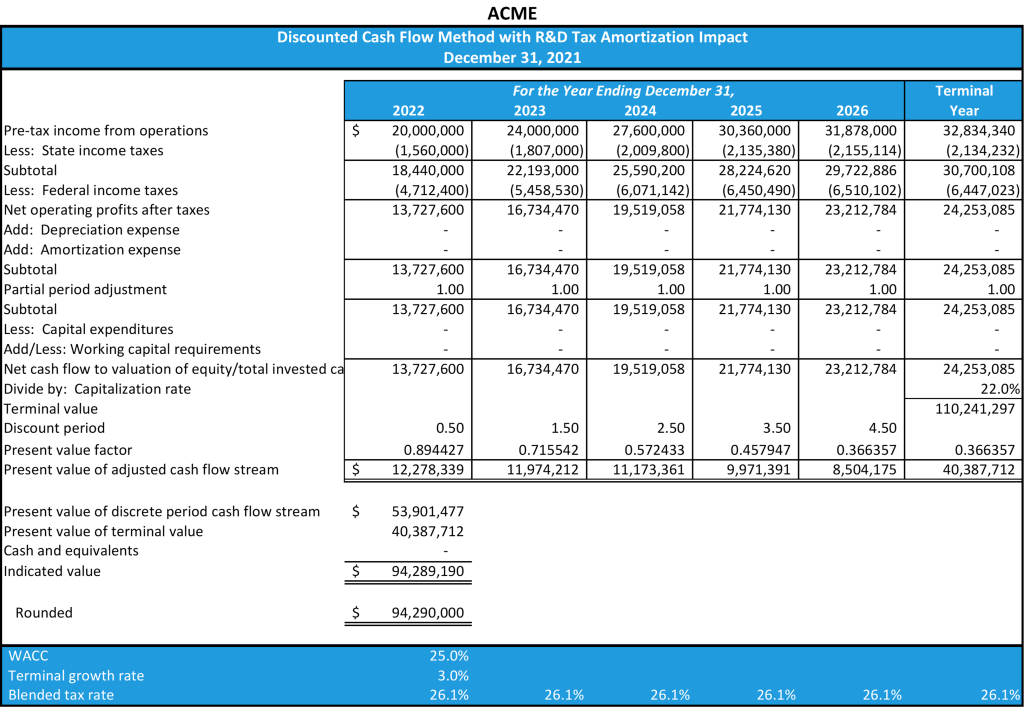

The income approach, particularly the discounted cash flow (DCF) method, is one of the most commonly used valuation methods in business appraisals. The DCF calculates after-tax cash flows of the business and discounts these cash flows at discount rate based on the cashflow’s riskiness. As shown in the examples, the higher tax obligations under the TCJA R&D tax laws reduce cash flows and, all else equal, reduce value. In our examples in Exhibits 2 and 3, the value differential is $2.5MM on a hypothetical value of approximately $100MM, a 2.5% valuation impact.

Exhibit 2

Exhibit 3

Domestic vs. Foreign R&D Spend

The examples above assume that all R&D expenditures are domestic. Many of our SaaS clients use a combination of domestic and foreign resources. Due to the longer amortization horizon (15 years for foreign versus five years for domestic), the cash flow impact is amplified in a scenario where R&D spend is non-domestic.