Home » Services & Solutions » Tax » Research and Development Credits

Research & Development Tax Credits

Many businesses qualify for Research & Development (R&D) Tax Credits without realizing it. Developing new products, improving manufacturing processes, creating software, or solving technical challenges may all qualify for valuable federal and state tax incentives.

LBMC helps businesses evaluate R&D activities, identify eligible expenses, and pursue available tax credits as part of a broader tax strategy. We work with specialized professionals to help clients maximize opportunities and meet documentation and compliance requirements.

Activities That May Qualify for R&D Tax Credits

Businesses often qualify when they are:

- Designing or improving products

- Developing software or technology

- Improving manufacturing processes

- Building prototypes

- Testing new materials

- Automating operations

- Solving technical or engineering challenges

- Improving product quality or efficiency

CHECKLIST: Do You Qualify for the R&D Tax Credit?

Many taxpayers tend to regard Research and Development (R&D) tax credits as an activity associated solely with high tech, biotechnology, and manufacturing companies, when in fact, many other day-to-day company operations qualify.

The purpose of R&D tax credits is to reward companies for investments in developing new or improved products, processes, or techniques; developing new technology, and developing and improving production/manufacturing processes.

Take a look at our checklist to gain insight into your business situation.

Find Out If You Qualify

Many organizations qualify for Research & Development Tax Credits without realizing it. A conversation with LBMC can help determine whether your activities may be eligible and what documentation may be needed.

LBMC's Research & Development Tax Credit Services

Research & Development Tax Credits are most valuable when they are identified accurately, documented thoroughly, and integrated into your overall tax strategy. LBMC helps businesses evaluate qualifying activities, calculate available credits, and support documentation that helps maximize available tax savings while reducing risk.

Qualification & Eligibility

Determine whether your business activities may qualify.

Many organizations perform qualifying research activities without realizing it. LBMC helps businesses evaluate products, processes, software development, and technical projects to determine whether they may be eligible for federal and state Research & Development Tax Credits.

Services include:

- Evaluation of research and development activities

- Eligibility assessments for federal and state R&D Tax Credits

- Review of product, process, and software development projects

- Identification of qualified research expenditures (QREs)

- Preliminary credit opportunity assessments

Credit Calculation & Documentation

Maximize available credits with well-supported documentation.

Once qualifying activities are identified, our team helps calculate eligible credits and develop documentation that supports your claim. Our approach is designed to provide accurate, well-documented credit calculations that align with IRS requirements.

Services include:

- Qualified Research Expenditure (QRE) analysis

- Federal and state credit calculations

- Technical interviews and project documentation

- Review of payroll, supply, and contract research expenses

- Documentation to support tax filings

Ongoing Advisory & Risk Support

Support your credit strategy with confidence.

Claiming the credit is only one step. LBMC helps businesses integrate Research & Development Tax Credits into their broader tax strategy while maintaining documentation that supports future reporting and potential IRS or state tax authority review.

Services include:

- Documentation retention recommendations

- Support during IRS or state tax examinations

- Annual credit updates and planning

- Coordination with Federal Business Tax planning

- Guidance as research activities evolve

Wondering If Your Business Qualifies?

Many organizations perform qualifying research and development activities without realizing they may be eligible for valuable tax credits. Talk to an LBMC expert to evaluate your opportunities and determine the next steps.

Why Choose LBMC for Research & Development Tax Credits

- A practical approach to identifying qualifying research activities, helping businesses recognize opportunities that are often overlooked during day-to-day operations.

- Coordinated technical and tax expertise that supports accurate credit calculations and well-documented claims aligned with IRS and state requirements.

- Integration with LBMC’s broader tax services, including Federal Business Tax and Credits & Incentives, to help maximize available tax-saving opportunities.

- Support throughout the entire process, from evaluating eligibility and documenting qualified activities to assisting with ongoing compliance and audit readiness.

- A trusted long-term advisor focused on helping innovative businesses capture available tax credits while supporting future growth and investment.

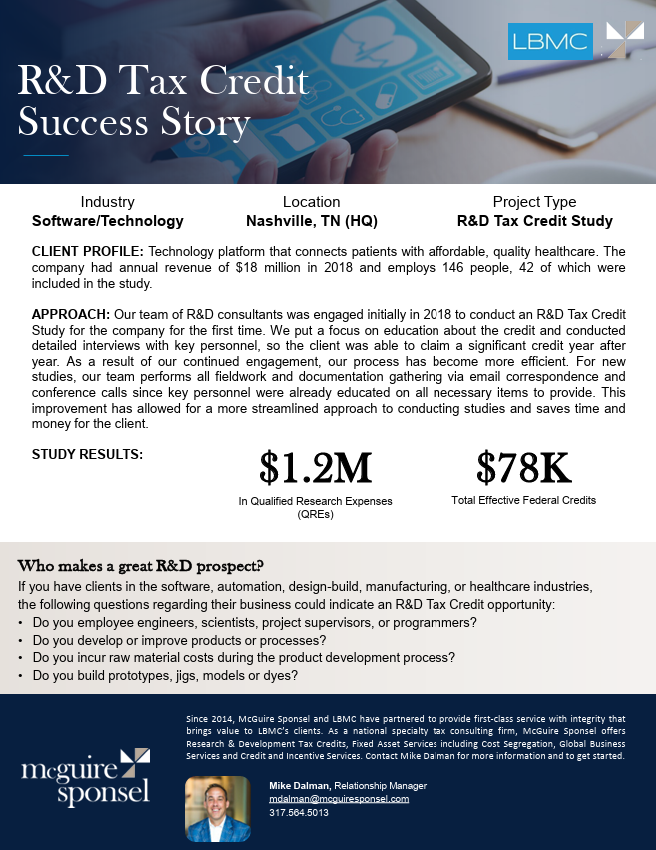

CASE STUDY: R&D Tax Credit for Healthcare Technology

This success story reviews a software/technology company located in Nashville, Tennessee that reached out to our team for an R&D Tax Credit Study. The Technology platform connects patients with affordable, quality healthcare. The company had annual revenue of $18 million in 2018 and employs 146 people, 42 of which were included in the study.

Approach

Our team of R&D consultants was engaged initially in 2018 to conduct an R&D Tax Credit Study for the company for the first time. We put a focus on education about the credit and conducted detailed interviews with key personnel, so the client was able to claim a significant credit year after year. As a result of our continued engagement, our process has become more efficient. For new studies, our team performs all fieldwork and documentation gathering via email correspondence and conference calls since key personnel were already educated on all necessary items to provide. This improvement has allowed for a more streamlined approach to conducting studies and saves time and money for the client.

Results

- $1.2 million in qualified research expenses (QREs)

- $78 thousand total effective federal credits

Industries We Support

Research and Development Tax Credits aren’t limited to laboratories or technology companies. Businesses across many industries qualify by developing new products, improving processes, creating software, or solving technical challenges. LBMC helps organizations identify qualifying activities and evaluate opportunities based on the work they already perform.

Explore our expertise in:

- Manufacturing & Distribution – Product development, process improvements, automation, and production efficiency.

- Technology & Software – Software development, platform enhancements, cybersecurity solutions, and emerging technologies.

- Healthcare & Life Sciences – Medical technology, healthcare innovation, diagnostics, devices, and process improvements.

- Construction & Engineering – Design-build projects, engineering solutions, custom fabrication, and construction innovation.

- Food & Beverage – Product formulation, manufacturing improvements, packaging innovation, and production processes.

R&D Tax Study Finds $133,064 in state and federal R&D tax credits for Contract Food Manufacturer

LBMC partnered with McGuire Sponsel to perform an R&D Tax Credit study for a contract manufacturer that specializes in developing new and improved formulations and manufacturing processes for the food industry. Our team identified $2,205,106 of Qualified Research Expenses (QREs). The resulting benefit earned $133,065 in total tax credits.Research & Development Tax Resources

- Research & Development Tax Credit: A Guide for Businesses

Discover how the federal Research & Development Tax Credit rewards innovation and helps businesses reduce tax liability while investing in growth. - How Manufacturers Benefit from the R&D Tax Credit

Learn how manufacturers can qualify for valuable R&D tax credits through product development, process improvements, and engineering activities. - Software Development and the Research & Development Tax Credit

Explore how software companies may qualify for the R&D Tax Credit when developing or improving software, applications, and technology solutions. - Understanding Qualified Research Expenses (QREs)

Learn which expenses qualify for the Research & Development Tax Credit and how proper documentation supports successful claims. - Section 174 Research Expense Capitalization

Understand how Section 174 impacts the treatment of research expenditures and what businesses should consider when planning for tax compliance. - One Big Beautiful Bill: Research & Development Tax Changes

Explore how recent federal tax legislation affects the deductibility of research expenditures and other provisions impacting innovative businesses.

Frequently Asked Questions About Research & Development Tax Credits

What types of activities qualify for the R&D Tax Credit?

Businesses may qualify when they develop or improve products, software, manufacturing processes, formulas, techniques, or other business processes that involve technical uncertainty and experimentation. Qualifying activities occur across many industries and are often part of everyday business operations.

Does my company need a formal research and development department?

No. Many businesses qualify without having a dedicated R&D department. Manufacturers, software developers, engineers, construction companies, and other organizations frequently perform qualifying activities while improving products, processes, or technologies.

What expenses may qualify for the R&D Tax Credit?

Qualified Research Expenditures (QREs) may include employee wages, supplies used during qualified research, and certain contract research expenses. Eligibility depends on the nature of the work performed and applicable tax rules.

How does the IRS determine whether activities qualify?

The IRS generally evaluates research activities using a four-part test that considers whether the work is technological in nature, addresses technical uncertainty, involves a process of experimentation, and is intended to develop or improve a product, process, software, or technique. LBMC helps businesses evaluate these requirements and document qualifying activities.

Can businesses claim credits for prior years?

In many cases, yes. Businesses that previously performed qualifying research activities may be able to identify unclaimed credits through a review of prior tax years, subject to applicable filing deadlines and tax rules.

How do Research & Development Tax Credits fit into an overall tax strategy?

Research & Development Tax Credits are often one component of a broader tax planning strategy. LBMC works with businesses to coordinate R&D credits alongside Federal Business Tax planning and other available tax-saving opportunities to help maximize overall value.

Meet Our Research & Development Tax Credit Team

LBMC’s Research & Development Tax Credit professionals help businesses identify opportunities to claim valuable tax credits for innovation, product development, software, engineering, and process improvements. Working collaboratively with our Federal Business Tax professionals and specialized technical resources, our team helps clients evaluate qualifying activities, document eligible expenses, and integrate Research & Development Tax Credits into their broader tax strategy.

Partner, LBMC India Professional Services, LLP, Leader in Chennai, India office and Shareholder, Tax Services, LBMC PC

Discover Your R&D Tax Credit Opportunity

Many organizations perform qualifying research and development activities without realizing they may be eligible for valuable tax credits. If your business is developing products, improving processes, creating software, or solving technical challenges, LBMC can help you evaluate available opportunities and determine the next steps.