Key Takeaways:

- Understanding Charitable Remainder Trusts (CRTs) and their importance in estate planning.

- Differentiating between Charitable Remainder Annuity Trusts (CRATs) and Charitable Remainder Unitrusts (CRUTs).

- Exploring the tax implications and benefits of CRTs.

- Identifying legal restrictions and potential pitfalls of CRTs.

- Practical advice on the creation and administration of CRTs.

What Are Charitable Remainder Trusts?

Are you looking for a way to reduce your tax burden while also leaving a lasting legacy?

Charitable remainder trusts (CRTs) might be the perfect fit. These irrevocable trusts allow donors to give assets to charity while also providing annual income for noncharitable beneficiaries, such as family members. CRTs are governed by a special section of the tax code and must meet specific requirements to function properly.

How Do Charitable Remainder Trusts Work?

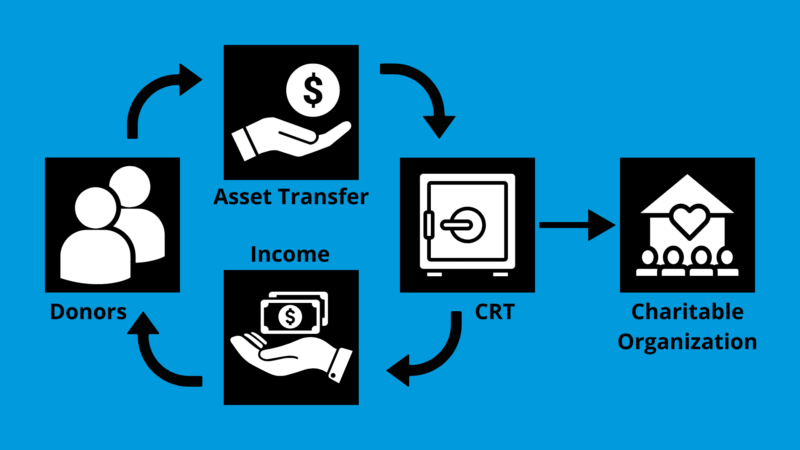

To create a CRT, a donor must transfer assets into an irrevocable trust instrument. Assets that can be donated to a charitable remainder trust include cash, stocks, real estate, private business interests, and private company stock (excluding S Corp stock).

For assets transferred during the lifetime of the donor, the trust’s basis is the same as it would be in the hands of the donor or carryover basis. The trustee receives the contributed assets, likely liquidates them, and then invests the proceeds for a tax-free return.

At least one living beneficiary is paid income from the trust, and the payments continue for the life of said beneficiary or a specific term of up to 20 years. As the name suggests, once the payment term ends, the remaining value of the trust transfers to one or more qualified United States charitable organizations.

Types of Charitable Remainder Trusts

There are two main types of CRTs, and the main difference is the payments to the noncharitable beneficiary remaining fixed or fluctuating.

Charitable Remainder Annuity Trust (CRAT)

The Charitable Remainder Annuity Trust (CRAT) provides fixed payments, meaning it pays beneficiaries a specific dollar amount each year that is at least 5% but no more than 50% of the fair market value of the assets originally placed in the trust. This type does not allow for additional contributions, so everything must be placed into the trust upon creation.

Charitable Remainder Unitrust (CRUT)

The Charitable Remainder Unitrust (CRUT) pays beneficiaries a percentage of the value of the trust each year. Since the fair market value fluctuates and the assets in the trust are revalued each year, these payments change year to year. CRUTs follow the same parameters mentioned above in that payments must be at least 5% but no more than 50% of the trust value but do allow additional contributions throughout the existence of the trust.

With both types, at least 10% of the initial fair market value of all property placed in the trust must be expected to pass to the remainder charitable beneficiary according to an actuarial analysis using an assumed growth rate dictated by the Internal Revenue Service. The CRAT has an additional restriction: the trust cannot have a great likelihood of paying out all of its assets to the non-charitable beneficiary(ies) before the remainder charitable beneficiary is allowed to receive them.

Why Create a Charitable Remainder Trust?

If an individual strongly supports a charitable organization, a CRT can help him or her easily plan significant contributions to said organization. They also allow one to provide a predictable income stream for the life of a noncharitable trust beneficiary or for a specific period.

One of the most attractive reasons to create a CRT is that they allow a donor to defer gains on the sale of assets transferred to the trust which in turn defers the income taxes on those gains.

A CRT may also provide a charitable deduction for contributions made to the trust. Charitable deductions are limited to the present value of the organization’s remainder interest calculated by taking the value of the contributed property minus the present value of the annuity or unitrust interest.

Tax Implications of Charitable Remainder Trusts

CRTs are tax-exempt under the tax code, but the trust’s annuity or unitrust payments to the noncharitable beneficiary(ies) are taxable to the beneficiary(ies).

Non-charitable beneficiaries are taxed on annuity and unitrust distributions of the trust in the following order: ordinary income, capital gains, other income, and corpus (principal of the trust). Payments are deemed ordinary income to the extent that the trust has ordinary income for the year or undistributed ordinary income from a prior year.

After the ordinary income is depleted, the payments are taxed as capital gains to the extent that the trust has capital gains for the year based on the sale of the trust’s capital assets or undistributed capital gains from a prior year.

After both ordinary income and capital gains are exhausted, then the payments are considered other income to the extent of the trust’s current year and accumulated other income including tax-exempt income. Once income of all types is totally distributed, the excess payments are considered trust corpus and not subject to income tax.

Filing Requirements with the IRS

As with all other financial vehicles, there is a requirement to report the activities of the trust to the IRS. The form used for CRTs is 5227, Split-Interest Trust Information Return. The focus is to report on the financial activities of the CRT for the year and properly reflect the distributions so the beneficiaries can report their income from the trust accurately. Beneficiaries must report payments received from the trust, detailed on Schedule K-1, on their personal individual income tax return Form 1040.

Legal Restrictions and Common Pitfalls

When creating a CRT donors must adhere to strict regulations, including:

- cannot inflate the basis of contributed assets to their fair market value to avoid capital gains or ordinary income tax,

- mischaracterizing distributions to avoid tax,

- giving a noncharitable beneficiary more than the annual income payment, and

- making an upfront payment to the charitable organization in lieu of the remainder interest.

Charitable trust donors may not pay personal expenses with trust funds, borrow from the trust, or change the character of payments from ordinary income to capital gains for the purpose of avoiding tax.

Pros and Cons of Charitable Remainder Trusts

Pros

The main benefit of a charitable remainder trust is its tax savings. The trustor receives a partial charitable deduction for his or her contribution to the trust, but may also notice reduced capital gains tax. Another advantage is that while planning to contribute to a charitable organization, the trust can provide a regular income stream to the noncharitable beneficiary.

Cons

The main pitfall is the irrevocable nature of the trust, which limits the donors’ access and control over the assets in the trust. On the other hand, the CRT is a complex legal structure requiring professional drafting and execution, making it expensive to administer. Potential donors may find it worthwhile to complete a cost-benefit analysis to see if a charitable remainder trust is the best way to use the assets that will be contributed.

LBMC Tax Team: Your Trusted Advisors for CRTs

Charitable remainder trusts are powerful tools in estate planning, offering tax advantages and supporting charitable goals. However, they require careful planning and adherence to regulatory requirements.

Curious whether a Charitable Remainder Trust is the right strategy for your estate planning? At LBMC, we specialize in guiding clients through the complexities of CRT creation and administration. Our team ensures you stay compliant while maximizing tax savings and charitable contributions.

Contact your LBMC tax advisor to discuss how a CRT might benefit your financial planning and assist with the necessary tax filing obligations.

Content provided by Ben Alexander. Ben Alexander is a Senior Manager in the Private Clients team working in the Knoxville office. He primarily works with high-net-worth individuals and their families regarding tax planning and related compliance. He also works in the areas of partnership, trust and gift taxation.

LBMC tax tips are provided as an informational and educational service for clients and friends of the firm. The communication is high-level and should not be considered as legal or tax advice to take any specific action. Individuals should consult with their personal tax or legal advisors before making any tax or legal-related decisions. In addition, the information and data presented are based on sources believed to be reliable, but we do not guarantee their accuracy or completeness. The information is current as of the date indicated and is subject to change without notice.