What Is an IC-DISC? (Definition and Overview)

An IC-DISC (Interest Charge Domestic International Sales Corporation) is a U.S. tax incentive that allows exporters to reduce federal income taxes by shifting export income to a tax-exempt entity. The IC-DISC earns a commission on export sales, and profits are distributed to shareholders at lower capital gains rates.

This structure is commonly used by manufacturers and distributors with export sales to create permanent tax savings.

An Interest Charge Domestic International Sales Corporation, or IC-DISC, offers a significant federal income tax savings for making or distributing U.S. products for export. It is not a tax shelter but creates permanent tax savings by transferring income from the exporter to the tax-exempt IC-DISC through an export sales commission. It’s an incentive specifically provided by the tax code that allows U.S. exporters to increase their ability to compete globally by reducing U.S. tax liabilities.

Key IC-DISC Takeaways

- Tax Efficiency: IC-DISC provides significant tax savings for U.S. exporters by transferring income to a tax-exempt entity, reducing overall U.S. tax liabilities.

- Commission Calculations: Commissions are based on export sales, calculated as either 50% of net income or 4% of gross receipts, offering a permanent tax rate advantage.

- Tax Benefits: Profits distributed as dividends are taxed at lower capital gains rates rather than ordinary income rates, decreasing tax costs for shareholders.

- Operational Impact: The operations of the exporting company remain unchanged by the existence of an IC-DISC, which is disclosed only to necessary tax authorities and advisors.

- Regulatory Stability: The Tax Cuts and Jobs Act did not alter IC-DISC regulations, maintaining its benefits despite broader tax law changes.

- Implementation Requirements: Proper setup includes timely election, compliance with stock and bookkeeping rules, and considering a domicile state without income tax for additional savings.

How Does an IC-DISC Work?

An IC-DISC structure is a separate entity that earns a “commission” on the operating company’s export sales based on the greater of

- 50% of net income on sales of qualified export property or

- 4% of gross receipts from sales of qualified export property.

A properly executed IC-DISC isn’t taxable at the entity level. So, the operating company receives a deduction for the commission paid at ordinary tax rates and the IC-DISC pays no tax.

It distributes all of its profits as qualified dividends, and the owners pay tax on the dividends at more favorable capital gains tax rates. Depending on the owners’ personal income levels, federal capital gains tax rates could be as low as zero or 15% — or as high as 23.8% (the highest federal capital gains rate of 20% plus an additional 3.8% of net investment income tax).

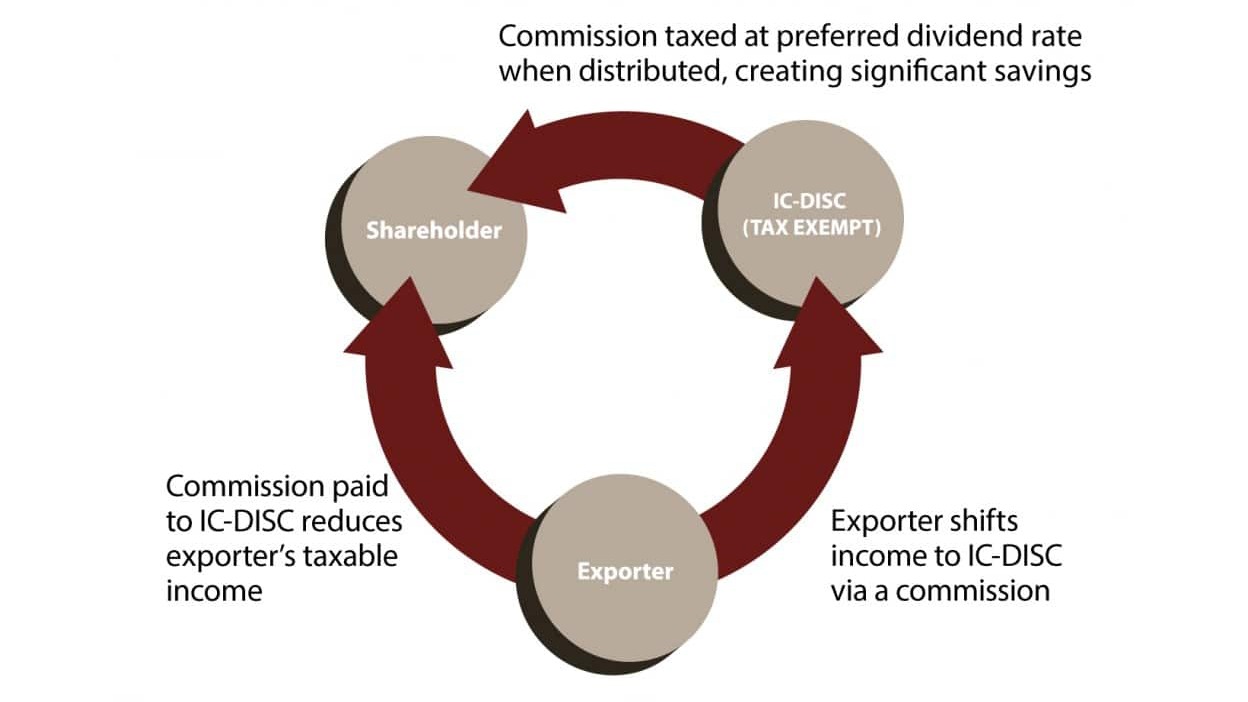

The IC-DISC commission payment reduces the exporter’s taxable income, thus reducing tax liability by the marginal tax rate of the commission amount. The commission is taxed at the qualified dividends rate only when distributed to shareholders as dividends. The transfer of income to the IC-DISC creates a permanent tax rate arbitrage on export sales, typically ranging from 15% to 18%.

An IC-DISC works by:

- “Calculating a commission on export sales (4% of gross receipts or 50% of net income)”

- “Deducting that commission at the operating company level”

- “Distributing profits as qualified dividends to shareholders”

Tax Benefits of an IC-DISC

Beyond tax reduction, an IC-DISC can be used to:

- Increase liquidity for shareholders or businesses.

- Supply ongoing financing to reduce cost of capital. An IC-DISC is not required to distribute all commission income to shareholders. In some cases, income can be loaned back to the exporter creating tax deferment and working capital.

- Create management and employee incentives for IC-DISC shareholders.

- Create a tax-advantaged vehicle for succession or estate planning. Income can be transferred to the IC-DISC tax free and then distributed in a tax-advantaged manner to shareholders. The distribution can provide funding for buyouts, or create a vehicle to transfer wealth at reduced effective tax rates.

- Eliminate double taxation for C-Corporations and defer taxes.

IC-DISC and the Impact of TCJA

The Tax Cuts and Jobs Act made no changes to the way an IC-DISC operates, but the introduction of the new qualified business income deduction (QBID) for pass-through entities and foreign-derived intangible income (FDII) for C-Corporations has reduced the overall IC-DISC benefit.

With the qualified business income (QBI) deduction scheduled to sunset after 2025 (absent legislative changes), many pass-through exporters may see the IC-DISC benefit increase again, often returning to mid-teen percentage savings.

Maximizing IC-DISC Calculations

Transaction-by-Transaction IC-DISC Calculations

In early discussions with potential clients, sales detail tends to be one of the most common hang-ups. Although the thought of collecting detailed sales information can seem like a tedious and overwhelming task, we generally see that companies already sufficiently track sales in a way that can be configured to run a transaction-by-transaction calculation.

The key behind a transaction-by-transaction calculation is in the detail provided by the client. The Code and Regulations allow us to modify the allocation of costs between domestic and export sales in an effort to either “maintain or gain” foreign market share. Thus, the general rule is the more detail we receive, the better we can model the cost allocations. Therefore, components of sales detail such as invoice number, product descriptions, product family, quantity, material cost, weight, square feet, and machine hours, provide more factors for us to model the calculation and maximize the commission expense.

Although accounting for sales can vary greatly from one company to the next, the sales detail the company currently maintains is always a great starting point. Often times this is plenty of information to run a transaction-by-transaction calculation. However, if you want to maximize your IC-DISC benefit, always remember: The more detail, the better!

Am I Utilizing the Best IC-DISC Ownership Structure?

Towards the end of the year, CPAs generally experience a spike in IC-DISC incorporations. This seasonal activity is understandable as clients want to have everything set-up and ready to go in order to maximize the IC-DISC’s prospective tax benefits for the upcoming year. Concurrent with these new incorporations comes the question of how to best structure the shareholder ownership of the IC-DISC. In its most basic form, there are two ownership structures that are utilized based on the exporting company’s entity type.

IC-DISC Structure for S Corporations and LLCs

The simplest ownership configuration for an IC-DISC comes when the exporting company is organized as a flow-through entity, an S corporation or an LLC. In this case, the IC-DISC is directly owned by the exporting S corporation or LLC as a subsidiary and the required movement of cash can flow in a complete circle back to the exporter. Under this scenario, at the end of the year the S corporation or LLC pays a commission to its IC-DISC subsidiary, and as soon as 24 hours later the IC-DISC subsidiary can pay those funds right back to the exporting parent in the form of a qualified dividend:

IC-DISC Structure for C Corporations

The other ownership structure utilized is where the exporting entity is a C corporation. This type of ownership structure is a classic brother/sister arrangement. Unlike the ownership structure of an S corporation or LLC, several Tax Code restrictions make direct C corporation ownership of an IC-DISC undesirable. But, both the C corporation and the IC-DISC could be owned by the same shareholders. In this type of structure, the C corporation will pay the deductible commission to the IC-DISC, thereby reducing its ordinary income, and the IC-DISC in turn pays that out to its shareholders in the form of a qualified dividend. Unlike the flow-through example discussed above, the money distributed to the shareholders as a qualified dividend permanently leaves the C corporation under this arrangement. However, the exporter has still effectively created a deductible dividend to the C corporation shareholder:

How LBMC Helps with IC-DISC Strategy

Whether the exporting company is structured as an LLC, S corporation, or C corporation, the LBMC and McGuire Sponsel team works with clients from initial evaluation through implementation to help determine the optimal IC-DISC structure and maximize tax savings.

Start Maximizing Your IC-DISC Benefits

IC-DISC can provide meaningful, recurring tax savings, but only when structured and calculated correctly.

If your organization exports U.S.-produced goods, you may be leaving significant tax savings on the table. Manufacturers and distributors with export sales exceeding $2.5 million are often strong candidates for an IC-DISC strategy.

Connect with our tax team today to evaluate your IC-DISC opportunity, optimize your structure, and maximize long-term savings.

IRS Resources

- IC-DISC Audit Guide

- Form 1120-IC-DISC Interest Charge Domestic International Sales Corporation Return

- Instructions for Form 1120-IC-DISC

IC-DISC FAQs

Will my customers know of the existence of an IC-DISC?

It is important to note that nothing changes for the exporting entity on a day-to-day basis. The best way to describe the existence of an IC-DISC is to think of it as if it were an internal sales agent that works entirely on commissions. When a sales agent sells a product, the exporting entity remains responsible to fulfill, invoice, and ship the order to its customers. Consequently, the exporter continues to operate its business in the same manner as if the IC-DISC were nonexistent.

If my customers find out about the IC-DISC, will they want some of the tax savings to be passed on through reduced prices?

The only individuals that will ever know about the existence of the IC-DISC is the IRS, their CPA firm, and the LBMC/McGuire Sponsel team. As mentioned above, nothing changes from the company’s operating standpoint and at no point would the supplier/commission agreement between the exporting company and the IC-DISC need to be disclosed to customers.

How much federal tax can it save?

To illustrate, let’s suppose Widgets, Inc. (a fictional S corporation) ships $2 million internationally and pays $80,000 in commissions to its IC-DISC. Assuming the owners qualify for the highest capital gains tax rate of 23.8%, they’ll owe federal tax of $19,040 on qualified distributions from the IC-DISC.

However, the owners also owe less tax on their S corporation earnings. Widgets can deduct $80,000 in commissions paid to the IC-DISC, resulting in a tax savings of $31,680, assuming that the owners are in the highest federal tax bracket of 39.6%.

The net savings is $12,640 ($31,680 – $19,040), or 15.8% of the commission charge. It’s often possible to pay a higher commission using the 50% of net export income calculation, however.

What steps are required to properly execute the IC-DISC strategy?

- Form the new IC-DISC entity under state law.

- Make the IC-DISC election within 90 days of formation.

- Offer only one class of stock with par or stated value of stock of at least $2,500.

- Maintain a separate set of books and records for the IC-DISC.

Taxpayers also can establish the IC-DISC in a domicile without state income tax to eliminate the need to file state income tax returns.

The IC-DISC primarily exists to calculate a commission on export sales, which is then returned to shareholders as a qualified dividend. Importantly, it is completely invisible to customers and the exporter reaps all the tax benefits.